What does market-leading cyber claims management look like? | Insurance Blog

Recently, many leading insurers have applied transformative solutions to enhance their cyber products. With the cyber insurance market projected to double to $29B by 2027, we explore what constitutes market-leading cyber claims management.

In this blog we’ll delve into the complexities of responding to cyber claims, the essential skills required by claims adjusters, and the measures insurers must take to achieve excellence in cyber claims management.

The complexity of cyber claims

The most comprehensive cyber coverage encompasses a broader range of perils than most other insurance products:

- First-party coverages: This includes damage to devices, network damage, physical property damage, and damage to digital assets. It also covers damage to or theft of intangible assets, theft of funds, and costs associated with recovery, restoration, and remediation. Financial losses due to business interruption, lost business opportunities, reputational damage, ransomware, and extortion are also included. Additionally, expenses related to investigations, notifying affected third parties, and damage to intellectual property such as patents and trademarks are covered.

- Third-party coverages: These coverages include contractual and legal liability, regulatory proceedings, and multimedia liability. They also encompass civil damages, compensation, payment card loss, errors and omissions, technology professional liability, miscellaneous professional liability, and network security and privacy liability.

When the policyholder of a comprehensive cyber product is a large multinational corporate business with both B2B and B2C customers, handling a potential large-scale claim becomes highly complex for claims adjusters. Cyber claims, akin to oil spillages, are catastrophic by nature, recognize no geographical boundaries, and are continuously evolving and unpredictable. Cyber breaches can critically impact businesses, societies, and essential national infrastructure, including hospitals, water and sewage systems, and airports.

The complexity, however, extends further. Cyber claims pose unique challenges to today’s claims adjusters due to the intricate technical nature of the claims, which involve IT systems, both tangible and intangible assets, cybersecurity protocols, digital forensics, and the constantly changing regulatory and legislative landscape concerning data protection, AI protection, and privacy law across all affected jurisdictions.

Furthermore, a cyber claims adjuster must be adept at instructing and managing a diverse group of specialists, ranging from IT forensic experts, data experts, and forensic accountants to credit monitoring experts, legal breach counsel, public relations experts, crisis management professionals, and ransomware attack experts.

The skills of a cyber claims adjuster

The skills of a cyber claims adjuster are multifaceted and require a detailed understanding of various aspects:

Knowledge Requirements: A cyber claims adjuster must possess advanced, industry-recognized qualifications and typically have a background in Errors & Omissions (E&O), Trade Credit, Political Risk, and/or Crisis Management. They need practical knowledge of applying first and third-party cyber coverages, reserving, evaluations, and risk management processes, usually gained from previous roles in cyber claims or broker advocacy.

Experience Requirements: The industry faces challenges due to a limited talent pool. It’s crucial for adjusters to understand the roles and responsibilities of various experts involved in cyber claims. Their practical experience is vital for effectively overseeing and managing these experts to ensure rapid response to claims, effective mitigation actions to prevent further losses, and complete resolution of claims. Cyber claims have grown in complexity and quantity, but many adjusters come from auxiliary lines of business. A key skill often missing is proficiency in IT systems, cybersecurity protocols, digital forensics, intangible assets, and a deep understanding of constantly evolving regulations and legislation across IT, AI, GDPR, and consumer privacy. This is particularly critical when insurance covers technology-based companies, where coverage is often bespoke and niche.

Operational Responsibilities: Adjusters must effectively determine the existence, cause, and scope of a breach and manage key activities in cyber claims management. This includes selecting and managing the appropriate incident response team, assessing ongoing or concluded breaches, evaluating the impact on the customer’s business and assessing breaches of cybersecurity protocols. It also covers responding in compliance with current data protection and privacy regulations, identifying and responding to fraud triggers, and providing feedback into underwriting risk controls and actuarial tables.

Customer Segment Knowledge: Proficient knowledge and experience with a range of customer segments, from SMEs to multinational and large corporate clients, are also essential for a cyber claims adjuster. Because Cyber is such a swiftly evolving product and still sub-scale to many other lines, insurers face the difficult question of whether to organize their Cyber claims team as a line of business CoE or whether to adhere to existing CoEs centred around SME, mid-market, multi-national clients etc.

Emerging risks and challenges

The task of determining the existence, cause, and scope of a breach is becoming increasingly complex due to the extensive coverage of cyber insurance, rapid technological and data platform evolution, the catastrophic and systemic risks associated with breaches, and the implications of Gen AI. Gen AI presents new opportunities and challenges, enhancing capabilities for both cyber attackers and defenders, leading to more sophisticated attacks almost daily.

The strategic choices to become market-leading in cyber claims

In conclusion, there are four key components to get right:

- Insurers need a claims application that supports the adjusters in effective management of the incident response team and experts. The application needs to be fit-for-purpose for cyber, which means a comprehensive master data management to orchestrate the 100+ relevant cyber claims data points as well as an expert-specific permission access to documents.

- Insurers need a comprehensive and continuous development program to remain proficient in evolving cyber risk, technology changes and especially the opportunities and challenges that Gen AI represent.

- Insurers need a comprehensive cyber saferoom that provides a secure space for pre-incident advice and training, incident response planning, notification services, etc. The saferoom must have the right guardrails that support collaboration with the independent legal breach counsel.

- Insurers need a continuous feedback-loop of claims master data that inform the actuarial tables and the risk controls in underwriting. Market-leading insurers achieve this with a scalable infrastructure and architecture, so that the technical pricing across all variables is informed in real-time based on loss history.

College Student Car Insurance Explained

A new school year is upon us. And it’s time for parents and students to discuss affordable car insurance for college students.

Whether you need to know about the cost of car insurance for college students, the discounts available for some, or the best types of car insurance for college students, the experienced team at Einsurance.com is here to help.

Education is expensive. And auto insurance topics can be confusing, we know. That’s why we provide these resources for consumers.

Keep reading for unbiased, honest information from real insurance agents on:

Right away, let’s answer your most important question.

Can I Keep My College Student on My Car Insurance Policy?

Sometimes, yes. If your child keeps your address as their primary residence, and drives a car insured as yours, they can stay on your policy.

Ultimately, if your college student is living at home and heading to the local community college, you don’t need to change much with your car insurance.

We still suggest that you:

- Review your policy to make sure you have the coverages you need (like theft or full coverage)

- Have a frank discussion with your child about safe driving and safe behavior on campus

But if your student is heading out of town — especially out of state, or to a major city — your insurer will likely require them to get a separate policy.

Don’t Mislead Your Insurer About Student Addresses

As insurance agents, we get several calls every year from parents who don’t know this, or who try to dodge the system. They often ask, “How does the insurance company know where my student lives or drives?”

When your child arrives at college, they’ll fill out paperwork for parking privileges. Insurers, the DMV, law enforcement and other organizations have access to those records.

Insurers also use more advanced technology. In 2024, they’re using satellite data, vehicle maintenance records, on-street photography and toll booth records to verify our driving habits.

New vehicles may also have the ability to record and send this information to legally qualified parties, like the DMV or insurance databases.

Ultimately, if your vehicle is parked at a college campus 1,000 miles away every day, your insurer will find out sooner or later. And if the vehicle is fully owned by, or leased by, the student, they may need their own policy.

College Student Car Insurance Basics

First, know the average college student in the US pays $2,500 to $5,000 for a full coverage policy. That equals about $210 to $425 per month that needs to be set aside in their budget.

Some college students will pay much more for a full coverage policy.

You can expect very high insurance costs if they:

- Have a poor driving history which includes DUIs or other serious charges

- Drive a very expensive vehicle

- Only recently got their license

- Have poor credit (in certain states)

- Have a history of claims or accidents

- Drive an electric vehicle (EV)

- Are male (yes, insurers do charge more to insure young males)

How Can I Save Money on College Student Car Insurance?

Right away, we see one way to save money on car insurance. Consider sending your student to school with an older, inexpensive car, and buying only liability coverage. This will likely cut your college student’s car insurance costs in half.

Consider a Cheaper Vehicle & Policy for Your College Student

It might feel expensive and risky to spend several thousand dollars cash for an older car that won’t be fully insured. However, if your college student is spending $5,000 per year on insurance alone, that’s $20,000 spent while getting a bachelor’s degree.

If your student plans on achieving a doctorate, they could spend $40,000 on auto insurance in eight years! An $8,000 used car will pay for itself several times in insurance savings. And it might be less likely to be stolen, when compared to a newer, expensive, popular vehicle.

If this purchase feels “pie-in-the-sky” right now, perhaps it’s best to send your college student to school without a car at all.

Don’t Forget About E-bikes, Scooters and Other Transportation Options

At Einsurance.com, we aim to match consumers with the right insurance for their needs, including college students and teens. But in the spirit of unbiased, full-disclosure, we must remind you that many students arrive at school without a vehicle, and that’s fine, too.

Part of their education is to learn how to live away from home; and understanding public transportation systems can be a valuable lesson. Our point is this, you don’t need to stress out about car insurance for college students.

Now, you may be thinking, “That’s great. But my child is studying abroad this year. What can you tell me about car insurance for international students?” Let’s find out.

Car Insurance for International Students

If your student is coming to the US for school, they will likely pay slightly more for auto insurance than students born here. According to our research, Geico, State Farm and Erie may offer the best rates for international students.

Also, your international student will need to apply for a new driver license. This is important, they won’t be able to buy car insurance without it.

If your child is heading overseas to study, they probably won’t bring a vehicle from home. The shipping expenses and risks make it difficult. Furthermore, your insurance policy will have little to no value outside the US.

Shopping for Car Insurance for College Students in Other Countries

Once your student arrives at school, they may wish to lease a vehicle or buy one, and they should shop around extensively for insurance.

Pro tip: Language barriers are inconvenient, and insurance is complicated in any language. Encourage your child to speak with translators or school advocates to help them get the best rates on car insurance overseas.

Studying overseas is an adventure and will bring many cultural lessons. One of them may be that autos are not needed for all lifestyles. In much of Europe and parts of Asia, many people choose to avoid vehicle ownership, because of the high costs and overall hassle. Your international college student may not even need to buy car insurance if they choose to live like a local.

Returning our gaze back home, let’s explore more about car insurance for college students living away from home.

Car Insurance for College Students Away from Home

We’ve already explained that your child may need to find their own car insurance policy if living away from home. You’re probably wondering, “Why?”

Know that insurance companies pay very close attention to claims made, thefts and college student behavior. Many parents are surprised when college student car insurance prices skyrocket because a student chooses to live and study in a city like New York or Los Angeles. Location everything, but there are still ways you can control your auto insurance costs.

In addition to buying an inexpensive car, or foregoing the vehicle entirely, your college student can:

- Pay a higher deductible (just remember, if there is a lienholder involved, they may require you to keep a certain deductible)

- Remove “bells and whistles” on a policy, like rental car coverage

- Pay off the vehicle entirely and buy a liability-only policy (though this comes with significant risk)

- Take a defensive driving course

- And look into discounts for college students

This leads nicely into our next section. Let’s explore some potential discounts on car insurance for college students.

Car Insurance Discounts for College Students

Car insurance companies know that college is a fun time for many students, and some may struggle to balance the social adventures with their responsibilities as students.

Put another way, it’s difficult to maintain excellent grades while partying hard or acting irresponsibly. And insurers always want their customers to behave responsibly.

That’s why many insurers offer good student discounts.

When shopping for car insurance for your college student, be sure to ask about these discounts, they can be significant! Usually, there is some reporting involved. Your student will need to send their grades to the insurer several times a year, and they must maintain a baseline GPA of 3.0 or higher.

Still, the savings are definitely worth the hassle. Trust us!

Next, let’s discuss how to shop for car insurance for college students.

How to Shop for College Student Car Insurance

If you’re a parent who already has car insurance, start by calling your current provider. They may offer you special discounts for your college student to gain their new business, and you might save more by bundling several policies together.

For example, some insurers offer dorm room insurance, renters insurance for off-campus housing and the like. They may offer some savings for buying these products together.

But don’t buy the first policy they quote! Be sure to shop around. Sometimes it makes good financial sense to use multiple insurance providers.

There are car insurance providers specifically marketing towards college students. These insurers will likely offer very attractive rates, because they hope to keep these customers for decades, as they become successful individuals with homes, families and more vehicles — all things that will need more insurance over the years.

Be sure to try our handy online quoting tool. Just enter your information and we’ll have auto insurers competing for your business right away.

Things You’ll Need to Get Car Insurance Quotes for College Students

Whether you’re shopping for car insurance for an international student, a student staying home, or one moving to the next big city, you’ll need certain documents/information on hand.

These include:

- The student’s full legal name

- Their new address (dorm building and room number, and school address)

- A copy of their driver’s license

- Title of the vehicle (if owned outright, or applied in some states)

- The vehicle identification number (VIN)

- A recent report card if applying for a good student discount

- Copies of defensive driving course certification if you have them

- Lienholder information (that’s the bank to which you make a car payment)

- Any other policies that might be relevant for bundling (dorm insurance, life insurance etc.)

If you already have car insurance for a college student, but you’re hoping to save money by shopping around, it helps to have the current policy on hand. This way, you can be sure you’re comparing “apples to apples” when it comes to:

- Deductibles

- Limits of liability

- Endorsements/riders

This leads to our next point, on how often one should shop for car insurance.

“How Often Should I Shop Around for Car Insurance?”

Whether you’re looking for auto insurance for yourself or for a loved one, you should shop around every few years. This could save you a ton of money over your lifetime, and it’s a valuable habit to teach your college student.

Know that insurers all tend to slowly increase your rates over time. This is true even if you’ve never made a claim, been involved in an accident, or gotten a traffic ticket. Insurers are in the business of making money, and even very safe drivers will experience rate increases.

Meanwhile, other insurance companies may be looking for customers just like you! And some insurers specialize in difficult risks, like drivers with a poor history or several DUIs. There is an insurer out there looking for your business, and we can help you find them.

We can also help you better understand the insurance products you buy every month. From life insurance to renters insurance, we cover it all.

Beyond premiums: What really drives customer loyalty? | Insurance Blog

Personal lines insurance is very price-sensitive. As discussed previously, maintaining a 20+% expense ratio is not feasible for insurers. Beyond pricing, what truly fosters customer loyalty, and how can insurers compete to increase their market share?

In this blog, I explore strategies for enhancing customer loyalty and retention, provide forecasts on the evolving risk landscape for auto and home insurance, and discuss Accenture’s predictions for how personal lines insurance buying behaviors might shift over the next decade.

The changing landscape of personal lines risk

Personal lines insurance has evolved from a specialty product to a digital commodity. Initially traded manually, it has now become a globally traded digital product. With around 4 billion vehicles and homes worldwide, personal lines insurance is both a global commodity and a constantly evolving risk.

The risk landscape varies significantly between auto and home insurance. Auto insurance covers a homogenous risk profile with approximately 600 common vehicle models globally. The rise of electric and autonomous vehicles is reshaping road regulations and vehicle repair processes and introduces new risks requiring product liability and cyber coverages.

Conversely, home insurance covers a heterogeneous risk profile with countless types of homes and building standards. The underlying home risk is significantly impacted by extreme weather that affects both frequency and severity of the damages. It’s fair to predict that extreme weather will not only impact ratings, but also building codes which would provide additional variables to price on.

While home and auto insurance represent key areas for personal lines insurance, consumers are also coping with the impacts of large-scale disruption – a volatile economic environment, residual impacts of the COVID-19 pandemic and the ongoing technology revolution have all shifted global dynamics significantly. Today, a consumer’s felt need for insurance is high, and the areas of risk that have them most concerned are shifting. We found that the rising cost of living and climate change were two top areas where consumers felt concerned about the risks but also least protected.

Generational shifts in insurance buying

The core consumers of insurance are changing. Millennials, the first generation of digital natives, are entering their peak insurance buying years. Insurers must cater to this demographic’s unique needs. Across all demographics, there is a demand for more, better, and faster services. Consumers want their unique needs met quickly and easily and are willing to share their data in exchange for a tangible better experience and product.

Strategic areas for enhancing value proposition

- Brand identity in customer interactions: Ensure that the brand identity is palpable in every customer interaction, creating a consistent and recognizable brand experience across all touchpoints.

- AI-augmented employees: Instead of focusing on implementing AI solutions, focus on augmenting employees with AI to provide more personalized and empathetic interactions, ensuring customers feel deeply understood. This is a fine, but critical nuance.

- Compelling digital experiences: Craft digital experiences that foster emotional connections. For instance, in travel insurance, offering dynamic updates on extreme weather, top tourist attractions, and local health advisories can significantly enhance customer engagement. Traditional risk mitigation notifications do not foster emotional connections with the customer.

- Real benefits for digital adoption: Ensure customers recognize tangible benefits from adopting digital channels, such as significantly faster resolution times and personalized digital interactions, making the digital shift worthwhile.

Creating compelling digital experiences for customers is key for enhancing customer loyalty. Recently, we worked with an insurer to address low engagement between agents and customers, insufficient customer information, and a lack of visibility for managing leads. The insurer and Accenture deployed an AI-enabled app to their customers; the app was incredibly intuitive and built using a scalable design for market adoption across Asia. The solution offered automated customer relationship management, marketing content recommendations, next-best-action recommendations, customer insights, 360 degrees customer insights, and agent performance management.

The results? 424% premium growth and 671% pipeline generated, proving that compelling digital experiences are worth their weight in gold.

Shifts in consumer buying channels

Traditional methods of purchasing insurance through brokers and agents are expected to decline in favor of direct sales and embedded insurance models. Munich RE have said that embedded insurance is projected to grow at a CAGR of 25% until 2030, potentially accounting for over US$ 500 billion in gross written premiums globally by 2030 for P&C lines.

Consumers show increasing interest in embedded insurance offers, where relevant risk protection is integrated into their purchase. For example, the share of consumers likely to buy auto insurance from a car dealer has increased from 32% to 42% since 2018. Consumers also want solutions beyond traditional home and auto insurance bundling, such as complete house buying services and home monitoring services.

Focus areas for insurers

- Performance and efficiency: Develop the best features and products.

- Experience and convenience: Delight customers with exceptional service.

- Solving, not selling: Play a relevant role in customers’ lives while creating value for all.

As the insurance landscape evolves, we must continue to harness the power of AI to turn challenges into opportunities. By empowering businesses with AI-driven solutions, we don’t just create tools – we transform possibilities into measurable success. In this journey of innovation, we redefine what’s possible, ensuring that the future of insurance isn’t just anticipated – it’s actively shaped.

Does Home Insurance Cover Water Damage?

Key Takeaways:

- Homeowners insurance policies typically cover water damage that occurs suddenly and accidentally, such as from burst pipes, appliance malfunctions, or storm-related roof damage.

- Gradual leaks and damage resulting from poor maintenance are generally excluded from coverage.

- It is crucial to thoroughly understand the specifics of your home insurance policy to know what types of water damage are covered and what are not.

In recent years, homeowners have increasingly faced the daunting challenge of water damage. This surge can be attributed to various factors, including extreme weather patterns, aging infrastructure, and the growing complexity of home appliances.

As water damage incidents become more frequent, understanding the intricacies of home insurance coverage has never been more critical. This comprehensive guide delves into the essential question: does home insurance cover water damage?

Whether you live in a single-family house, a mobile home, or a condo or townhouse (where an association policy may be primary), there is insurance coverage that addresses water damage. We’ll explore different scenarios, from rain and plumbing to roof leaks and mold, providing you with valuable insights and practical tips for managing water damage insurance claims.

Understanding Home Insurance Coverage for Water Damage

Home insurance policies are designed to protect homeowners from a myriad of risks, including water damage. However, the specifics of this coverage can be complex and often vary between policies. Generally, standard home insurance policies cover sudden and accidental water damage, such as that caused by a burst pipe or an unexpected appliance failure.

Sudden and accidental water damage—usually covered under most standard homeowners insurance policies—refers to unexpected events, such as a burst pipe or an appliance failure that causes immediate and significant water damage to your property. The key aspect of this coverage is the sudden and accidental nature of the incident, which means the damage must have occurred without warning and as a result of an unforeseen event.

This type of homeowners coverage can provide financial relief for repairs and restoration, ensuring that you are not burdened with the full cost of unexpected water damage, which can include things like carpet and drywall replacement, as well as personal property, like furniture, appliances, clothes, and more.

What About Leaky Faucets and General Disrepair?

In contrast, gradual leaks and maintenance issues are typically excluded from standard homeowners insurance policies. These exclusions pertain to damages that occur slowly over time, such as a slowly dripping pipe or roof leaks that develop due to neglected maintenance.

Insurance companies consider these types of issues preventable and within the homeowners control to address before they cause significant damage. Consequently, damages resulting from lack of maintenance or wear and tear are not covered, leaving homeowners responsible for the costs of repairs.

Get to Know Your Policy Before You Need It

Understanding the specifics of your insurance policy is crucial to preventing unpleasant surprises when filing a claim. Familiarizing yourself with the terms and conditions, including what types of water damage are covered and excluded, can help you take proactive measures in maintaining your property and ensuring adequate protection.

It goes without saying, regular maintenance and timely repairs can go a long way to mitigate the risk of damage that is not covered by insurance, providing peace of mind and financial security.

Does Home Insurance Cover Water Damage from Rain and Flooding?

Rainwater damage is covered by most standard homeowners insurance policies if it results from a covered peril. This means that if rainwater enters your home due to an event such as a windstorm that damages your roof or windows, your policy will likely cover the resulting water.

The key factor is that the rainwater must have entered due to a specific incident that is listed as a covered peril in your policy. This can include situations like a tree falling on your house during a storm or shingles being torn off by high winds, allowing rain to penetrate your home.

How Does Flood Coverage Differ?

However, flood damage is not typically covered under standard homeowners insurance policies and requires a separate flood insurance policy. Flood insurance is essential for protecting your home and belongings from the potentially devastating effects of floodwater. Flooding, which is defined as water inundating normally dry land from sources like rivers, lakes, or heavy rainfall, necessitates additional coverage through the National Flood Insurance Program (NFIP) or private insurers. Assessing your flood risk is a crucial step in determining whether you need additional coverage.

Factoring in the growing threat of worsening storms and climate upheaval, consider things such as your home’s proximity to bodies of water, the local topography, and historical flood data. Even if you do not live in a high-risk flood zone, flood insurance can provide valuable protection, as floods are becoming more common in previously unthreatened areas.

Does Home Insurance Cover Water Damage from Appliances and Plumbing?

Modern homes are equipped with a variety of appliances and plumbing systems that, while convenient, can also be potential sources of water damage. From washing machines to dishwashers and water heaters, a malfunction can lead to significant water damage. So, does home insurance cover water damage from appliances and plumbing?

Sudden and accidental damage from appliances and plumbing is typically covered under most standard homeowners insurance policies. This coverage includes incidents such as a washing machine hose suddenly bursting, a dishwasher leaking unexpectedly, or a pipe freezing and then bursting.

These types of events are considered unforeseen and occur abruptly, causing immediate and significant damage. Insurance policies generally provide financial protection for the repairs and restoration needed to address the damage caused by such sudden and accidental occurrences.

Maintenance is Key to Avoiding a Problem

Regular maintenance is crucial to prevent non-covered gradual leaks. Insurance policies often exclude damage that results from a lack of maintenance or from gradual wear and tear. This includes slow leaks from appliances or plumbing that deteriorate over time due to neglect.

Homeowners are responsible for the upkeep of their property, and routine maintenance can help identify and fix minor issues before they escalate into significant problems. Regular inspections and timely repairs are essential in preventing leaks that develop slowly and ensuring that your home remains in good condition.

Document Maintenance and Repairs…Just In Case!

Documenting appliance maintenance can significantly support your insurance claims. Keeping detailed records of maintenance activities, such as service receipts, inspection reports, and repair logs, can demonstrate that you have taken proactive steps to maintain your appliances and plumbing systems.

In the event of a sudden and accidental damage claim, this documentation can provide evidence that the damage was not due to neglect or poor maintenance. This can help streamline the claims process and increase the likelihood of your claim being approved, providing you with the necessary financial assistance for repairs.

Does Home Insurance Cover Water Damage from Roof Leaks?

A leaky roof is a homeowners nightmare, and it often raises the question: does home insurance cover water damage from roof leaks?

The answer depends largely on the cause of the leak. If a roof leak is caused by a covered peril, such as a storm or falling tree, the resulting water damage is typically covered by home insurance.

However, if the leak results from wear and tear or lack of maintenance, the damage may not be covered. It’s essential for homeowners to perform regular roof inspections and maintenance to ensure their roof remains in good condition and to understand the terms of their insurance policy.

Does Home Insurance Cover Water Damage and Mold?

Mold resulting from covered water damage events is typically included in standard homeowners insurance policies. If mold growth occurs due to an insured peril, such as a burst pipe or sudden appliance leak that is promptly addressed, the cost of mold remediation and repairs is generally covered.

Insurance policies recognize that mold can develop quickly after an unexpected water damage event, and they provide protection for the cleanup and mitigation necessary to restore a safe living environment.

However, mold resulting from long-term moisture issues is usually not covered. This includes mold growth caused by ongoing leaks, high humidity, or neglected maintenance over an extended period.

Insurance companies consider these scenarios preventable and within the homeowners responsibility to address before they become significant problems. As a result, damages from mold due to chronic moisture issues are often excluded from coverage, leaving homeowners to bear the financial burden of remediation and repairs.

Prompt action and preventive measures are crucial in mitigating mold risks. Addressing water damage immediately, thoroughly drying affected areas, and repairing any leaks or moisture sources can prevent mold from developing.

Regular inspections and maintenance, such as checking for leaks and ensuring proper ventilation, can also help prevent conditions conducive to mold growth. By taking proactive steps, homeowners can reduce the likelihood of mold issues and ensure that any mold that does occur due to covered events is managed effectively.

Water Damage Insurance Claim Tips

Filing a water damage insurance claim can be a daunting process. To ensure a smooth and successful claim, it’s important to follow certain steps and best practices, including:

- When dealing with property damage, it is essential to document the damage thoroughly with photos and videos. This visual evidence can provide a clear and detailed account of the extent and nature of the damage, which is crucial for supporting your insurance claim. Ensure you capture all affected areas and items from multiple angles and include close-up shots of specific damages. This documentation will be invaluable when assessing the damage and verifying your claim with the insurance company.

- Report the damage promptly to your insurance company to initiate the claims process as quickly as possible. Most insurance policies require timely reporting, and delays can potentially affect the outcome of your claim. Provide all necessary details and submit the documented evidence to your insurer, facilitating a smooth and efficient evaluation process.

- Make temporary repairs to prevent further damage and keep receipts for all expenses incurred. Taking immediate steps to mitigate additional damage, such as covering broken windows or tarping a damaged roof, is not only practical but often a requirement under your insurance policy. Save all receipts for materials and services used in these temporary repairs, as they may be reimbursable under your claim.

- Understand your policy’s coverage limits and deductibles to manage your expectations and financial responsibilities.

Familiarize yourself with the specifics of your policy, including the maximum coverage amount and the deductible you must pay out-of-pocket before insurance coverage kicks in. Knowing these details will help you better navigate the claims process and ensure you are adequately prepared for any expenses not covered by your insurance.

Finally—the Importance of Understanding Your Coverage

Homeowners insurance can provide crucial protection against various forms of water damage, but understanding the specifics of your policy is essential. Coverage typically includes sudden and accidental damage caused by incidents such as burst pipes, appliance malfunctions, and storm-related breaches.

These unexpected events can cause significant and immediate harm, and insurance policies are designed to help mitigate the financial impact of such occurrences by covering necessary repairs and restoration.

However, it is equally important to be aware of the exclusions within your policy. Gradual leaks and maintenance issues, which develop over time due to neglect or lack of upkeep, are generally not covered. This means that homeowners must take responsibility for regular maintenance and prompt repairs to prevent these types of damages.

Similarly, mold resulting from long-term moisture problems is usually excluded from coverage, emphasizing the need for proactive measures to manage humidity and address potential water issues before they escalate.

Document, Document, Document

To maximize the benefits of your homeowners insurance, prompt action and thorough documentation are key. In the event of water damage, document the damage extensively with photos and videos, report it immediately to your insurance company, and make temporary repairs to prevent further harm. Keeping receipts for these repairs can support your claim and ensure you are reimbursed for out-of-pocket expenses.

Additionally, understanding your policy’s coverage limits and deductibles will help you navigate the claims process more effectively and be better prepared for any uncovered expenses. With the right knowledge and preparation, you can navigate the complexities of home insurance and safeguard your home against the unexpected challenges posed by water damage.

Contact einsurance.com to get quotes on home insurance or home and auto insurance bundles today.

5 areas of algorithmic underwriting advantage | Insurance Blog

Use of algorithmic underwriting is increasing across the insurance industry. With enhanced decision-making and improved risk assessments, an algorithmic approach to underwriting can optimize operations for insurers and experience for their customers.

In this post we delve into the evolution and advantages of algorithmic underwriting and share our insights on building and scaling an algorithmic underwriting platform.

The evolution…

Algorithms have always been part of the underwriting process, but they have generally been restricted to rating. For example, in determining risk factors for car insurance, algorithms, or mathematical formulas, would be used to set rates based on vehicle make, model, driver age, location and previous history. Whether simple or complex, algorithms have long been our core rating tool.

The use of algorithms in other areas of the underwriting process has been limited due to fear of overlapping these factors with rate making, or simply the lack of data and analytical capabilities at other parts of the underwriting process to make these decisions. Instead, the insurance industry has typically depended on complex rules engines for decisions on risk acceptance, risk tiers and report ordering.

With advancements in data access and analytics tools, carriers are now rethinking the use of algorithms, using them either alone or alongside traditional rules engines, to enhance decision-making throughout the underwriting process.

How it works…

Algorithmic underwriting employs analytical models to automate decision-making in the underwriting process or to provide insights to assist underwriters. For more homogeneous risks, it can fully or partially automate underwriting.

Key decisions made using algorithmic underwriting:

- Determining if a submission fits the carrier’s risk appetite

- Identifying key risk characteristics such as the correct SIC/NAIC code

- Prioritizing accounts based on desirability and winnability

- Making risk determinations on portions or the entirety of risk

Through this approach, carriers can achieve faster risk acceptance or rejection and reduce underwriting workloads. It also helps in providing customers more personalized risk assessments, real-time risk management and a seamless experience.

5 advantages of algorithmic underwriting

Algorithmic underwriting significantly benefits the insurance industry across 5 key areas:

- Process efficiency: By automating the underwriting process, we are seeing algorithmic underwriting reduce processing times by up to 50%, streamline operations, increase testing speed and simplify the maintenance of complex decision-making systems. In addition, the automated processes of algorithmic underwriting can help handle an increase in applications reviewed by up to 25%, enabling insurers to increase premium without additional operating costs.

- Accuracy: The accuracy of risk assessments can be improved through analysis of more extensive data sets. These analyses help identify patterns and correlations that might be missed by human underwriters alone. With this augmentation of the underwriter’s insight and judgement, errors in risk assessments can be minimized and fraud can more easily be detected. We estimate fraud losses may be reduced by up to 30% for some insurance companies.

- Price: Pricing decisions can be more accurate by enhancing risk assessments. Algorithmic underwriting helps tailor premiums to individual risk profiles, enhance customer satisfaction and competitiveness. Additionally, it supports dynamic pricing, adjusting premiums in real-time based on changing risk factors, which we see improving underwriting profitability by up to 20%.

- Proactive risk management: Algorithms can help insurers proactively identify emerging risks and adjust their underwriting and risk management strategies. This can help to mitigate potential losses, reduce loss ratio and improve overall portfolio performance.

- Customer experience: Algorithmic underwriting allows for instant or near-instant decisions on coverage eligibility, pricing and personalized offers. With predictive and prescriptive analytics, insurers can make real-time, contextualized offers, making insurance more accessible and relevant to the individual customer’s needs. It also makes insurance more attainable to customers or segments that may have been marginalized by underwriting methods of the past.

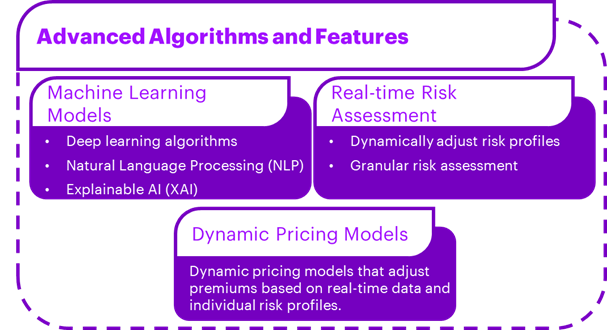

Building an algorithmic underwriting platform at scale

An algorithmic underwriting platform requires a multi-layered approach that takes future scalability into consideration. Advanced features needed when considering an algorithmic underwriting platform include machine learning models, real-time risk assessment, and dynamic pricing models.

Challenges to consider as you optimize your data and algorithmic underwriting platform:

- Data quality and availability: Data may be fragmented, incomplete or outdated.

- Model interoperability: Complex machine learning algorithms used for underwriting may lack transparency and interoperability making outcomes difficult to explain.

- Compliance: As regulation of algorithmic models and AI increases, insurers must stay ahead of the guidance and adjust models as needed.

- Fairness and bias: If not proactively addressed, algorithmic underwriting presents the risk of perpetuating unfair practices and historic biases.

- Data privacy and security: Algorithmic underwriting involves collecting, processing and storing large volumes of personal and sensitive data. Securing customer data is vital for compliance and maintaining customer trust.

Success stories…

We see examples of success with algorithmic underwriting across the industry. In P&C for example, Ki Insurance leverages AI and algorithms for instant commercial insurance quotes and automated policy issuance. Hiscox collaborated with Google Cloud to develop and AI model that automates underwriting for specific products. Meanwhile, on the life insurance side, ethos employs machine learning to asses risk and to offer simplified insurance applications.

Conclusion

While algorithmic underwriting is not a novel concept in insurance, it is revolutionary in its enhancement of access to new data sources, improved data quality and better analytics tools. These enhancements allow underwriters insight from other areas of the value chain and extend their capability beyond archaic models or knockout rules.

Despite their sophistication, insurers will need to be aware of the potential for bias and a lack of transparency in algorithmic underwriting models. Ethics and compliance, including data privacy, consumer protection and fair lending laws will pose challenges for insurers to address from the outset.

As technology continues to evolve and data analytics capabilities expand, we bear witness to how algorithmic underwriting will revolutionize the insurance industry, drive innovation and empower financial institutions to make more informed, data-driven decisions.